Dream Homes, Smart Loans: Navigating Vacation Home Financing for Airbnb Hosts

There’s nothing more fulfilling than making your dream home come true.

When it comes to achieving this goal, securing an Airbnb property can be your best bet. Not only does it help realize your dream buy a vacation home, but this property type can also be your short or long-term rental business.

So, how can you make your dream home utterly realized? Getting a smart loan is the answer!

In this article, we’ll take a closer look at the vacation home market and Airbnb financing. As an Airbnb host, learn more about the following:

- Why you should apply for financing;

- What financing options are available; and

- How to secure the right Airbnb loan.

Ready? Let’s dive right in!

A Closer Look at the Vacation Home Rental Market and Airbnb Financing

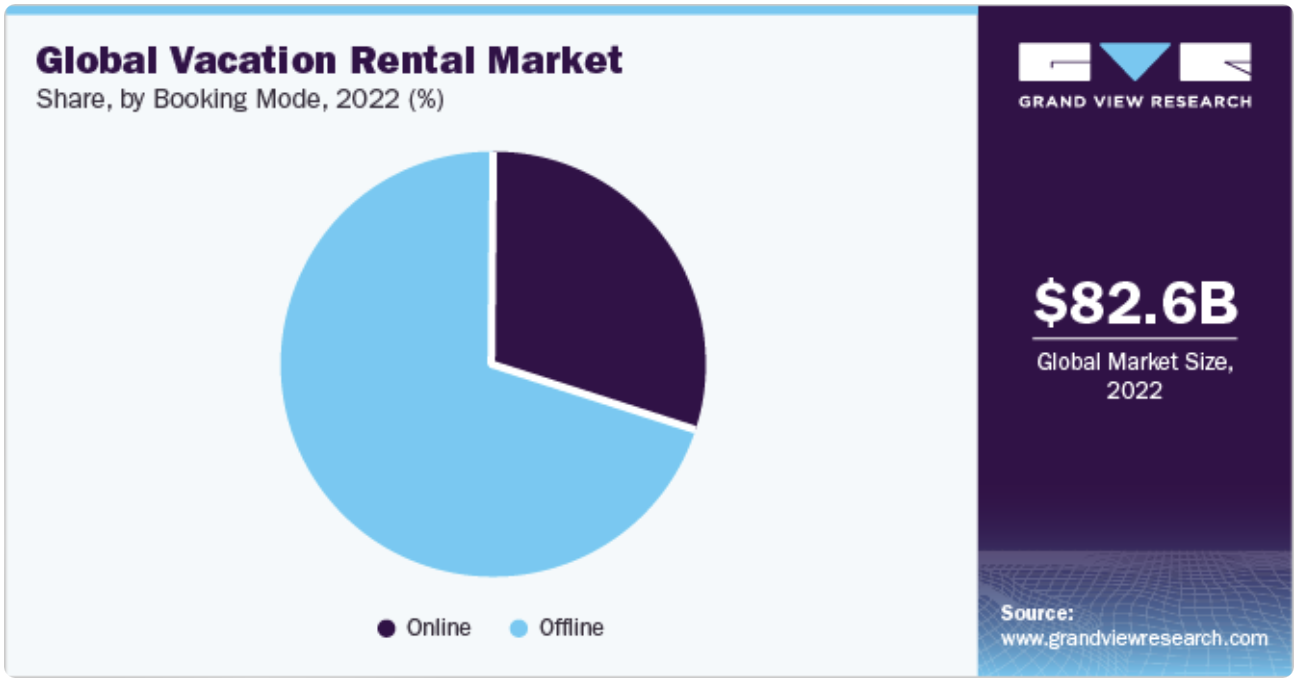

The vacation home rental market has been booming. Taking up space in vacation homes has become increasingly popular across the globe. Take it from the recent Grand View Research report:

The global vacation rental market size is projected to grow from $82.63 billion in 2022 to $.119.01 billion by 2030. It’s forecasted to achieve a compound annual growth rate (CAGR) of 4.7%.

Enter Airbnb, the leader in the vacation rental industry. Airbnb all started back in 2007 when roommates Brian Chesky and Joe Gebbia rented out the living room of their apartment in San Francisco.

Airbnb soon expanded after having gone overseas with its first operation in Hamburg, Germany. It was only in 2020 that it became public after having started as a private company. In 2022, its global revenue hit $8.4 billion—and the rest is history!

According to Ruby Home Luxury Real Estate, Airbnb tops the industry list with about seven million listings in 220 countries, followed by Booking.com (with over six million listings) and Expedia (with two million listings).

Understanding what Airbnb financing entails

Given the growth of the vacation rental market, it’s a good idea to capitalize on it and invest in an Airbnb property. Then, you can put the property out in the real estate market for short- or long-term vacation home rental.

But what if you don’t have enough capital to purchase an Airbnb property? That’s where the vacation home loan financing enters the real estate scene.

For the uninitiated, Airbnb financing entails securing a loan from a bank, government agency, or other financial institution to buy an Airbnb property for rental business.

Airbnb loans are specifically designed for rental property investors looking to purchase a property to rent out on the Airbnb platform. Take note that Airbnb financing comes:

- In various types;

- From different lenders;

- At varied costs; and,

- With different terms.

Top reasons to apply for Airbnb financing

Now, you might be wondering what the value of Airbnb financing is. For the most part, you take this option when you need to buy a property since you don’t have the money to pay it in full.

But as an Airbnb host, you can get a loan to furnish or renovate your existing property. You can also do this to take advantage of your equity, launch a rental business, or cover your operating expenses.

That said, here are the top reasons Airbnb hosts seek proper financing:

Purchase a property

Of course, you want to make your dream home come true by buying the best Airbnb property. From there, you can turn it into your vacation house and rent it out from time to time.

Capitalize on the equity

If you have an existing mortgage, you might want to take advantage of your home equity. As an Airbnb host, you can use the lump-sum money to remodel your property or invest in a new house for another rental business.

Renovate your property

As an Airbnb host, you need to stay on top of your rental property upkeep. If you need money for home repairs, improvements, or upgrades, then getting a loan would help.

Start a rental business

As mentioned, Airbnb financing helps you buy a new property for your Airbnb rental business. If you already own one, you can have a second mortgage to expand your real estate business as an investor.

Finance operating costs

As an Airbnb host, you deal with a lot of expenditures. Think of marketing and advertising expenses, house cleaning fees, property maintenance costs, and even the wage of your property manager for Airbnb management. If you fall short on this, you can always seek financing.

Find out what Airbnb financing options are available in the next section.

Home Financing Options for Airbnb Hosts

Investing in an Airbnb property is a wise business decision. Not only does it let you own a house, but it also allows you to secure a property for your rental business.

But before you reap the benefits of your investment properties and Airbnb rental business, you must first seek funding for your property purchase. Explore some of the financing options below:

Conventional mortgage:

This mortgage type is a long-term loan offered by a bank backed by Freddie Mac or Fannie Mae but not supported by government agencies like FHA, VA, or USDA loans. You can get a conventional loan for your Airbnb investment property as you would with a home purchase, whether with a fixed-rate mortgage (FRM) or an adjustable-rate mortgage (ARM).

Home refinancing:

As the name suggests, home refinancing entails securing a new loan with a different term from a different lender to finance your Airbnb property. Some Airbnb hosts take this option to get a better deal, like a lower interest rate, a shorter loan term, or a switch from ARM to FRM.

Debt-service coverage ratio (DSCR) loan:

The DSCR loan for Airbnb is a type of financing where you get qualified based on the ratio between your property’s net operating income (NOI) and the money you plan to borrow. This loan type is typically for investors looking to furnish or renovate their Airbnb properties. However, it can also be a long-term loan for purchasing an investment property, albeit with stringent requirements.

Home equity loan:

This loan type allows you to access the equity on your primary mortgage for your first property to buy a second home. Considered a second mortgage, it lets you borrow a lump sum of money from the equity to finance your Airbnb property. Note, however, that a home equity loan comes with a high risk since it’s tied up with your first mortgage.

Home equity line of credit (HELOC):

HELOC works somehow the same as a home equity loan since it’s also a second mortgage. However, it gives you access to cash for a particular time (usually about ten years), called a draw period, after which the loan repayment starts. You can borrow against a line of credit to buy an Airbnb property or renovate your existing one.

Small business loan:

As the name implies, this loan type entails borrowing money from a lender to finance your small business. This loan applies to your Airbnb rental business since you’re looking to invest in a property to rent it out for money. Many startups and small businesses apply for Small Business Administration (SBA) loans offered by the government.

Hard money loan:

This short-term loan is readily available for real estate investors who haven’t qualified for traditional loans, such as those mentioned above. For instance, you can borrow money from an individual or less-institutionalized lender to invest in an Airbnb property if you have a poor credit score. However, be prepared for a higher down payment and interest rate.

As you can see, you have various options for financing your Airbnb property purchase. But how can you make an informed real estate decision?

Discover practical tips for choosing the best financing option for your Airbnb property in the next section.

How To Secure the Right Airbnb Financing

Earlier, you’ve learned much about what Airbnb financing entails and what loan options are available. Now, it’s time to know how to secure the proper funding for your Airbnb property.

Follow our crucial steps below:

1. Study the local Airbnb market

The initial step is to study the vacation home rental market in the area where your potential Airbnb property resides. This move is particularly crucial if you’re looking to buy a house for the first time and rent it out thereafter. More so if you’re planning to refurbish, remodel, or renovate your existing vacation rental property to keep up with the market trends.

Adam Garcia, Owner of The Stock Dork, advised performing due diligence for your Airbnb property investment. “Before you select a prospective house and seek proper funding, you must ensure it’s worth doing so. Is the vacation home rental market thriving in your locality? Will buying an Airbnb property in this area pay off in the long run?”

2. Assess your financial health

After studying the vacation home rental market, you can start examining your mortgage rate and finances. You’re seeking financing because you aren’t able to pay it in full. But the most critical question is: Can you repay it for the long term?

That said, assess the following:

Financial status:

It’s best to evaluate your current financial situation to see how much you need for your Airbnb loan. Do you have enough savings and an emergency fund in place? Does your household income give you access to social security benefits and financial assistance?

Income source:

Of course, you should assess where your money comes from, whether from your regular employment or business venture, to ensure a steady rental income stream. That should allow you to repay your loan for the long term.

Financial expenses:

Not only do you have to look at your rental income, but you also need to examine your expenditures. Think of the food expenses, transportation costs, and regular bills you pay. Consider your children’s education, lifestyle expenditures, and other future expenses that might impact your loan repayment.

Credit score:

Finally, focus on your credit score, as this will determine your lender’s approval or denial of your loan. That will also help you decide what type of financing to obtain for your Airbnb property investment.

3. Request quotes and compare loan options

At this point, you must be fully decided to invest in an Airbnb property and obtain a loan. Then, it’s time to look for prospective lenders that can give you the best deal. While doing your research, start requesting loan quotes from different lenders. From there, take ample time to review and compare financing options.

Harry Anapliotis, Writer at Rental Center Crete, suggests reviewing various loan options. “You should be highly critical of what these lenders bring to the table. Aside from the loan amount, check the loan term, down payment, interest rate, monthly contractual payment (MCP), and escrow account, whether tax or insurance. If possible, consult a real estate expert to help you make an informed decision.”

4. Consider all expenditures involved long-term

Let’s go back to the original premise: You are seeking financing to purchase a property for your Airbnb rental business. This means that you might be able to have cash reserves buy this property and rent it out thereafter. However, you are responsible for repaying the loan for a certain period of time.

Here’s the catch: Aside from the monthly contractual payment (MCP), you should come prepared for all your Airbnb rental income and business expenditures. You probably have a vacation rental inventory checklist, not to mention all related expenses, such as the following:

- Property inspection and appraisal: There are instances when you need to inspect your Airbnb property and assess your vacation home value. Unfortunately, property inspection and assessment come with prices. They are something you must come in financially ready for!

- Regular upkeep and cleaning: Once you have the rental property in place, you’ll be responsible for cleaning and maintaining the property. Therefore, you better be ready for Airbnb cleaning fees and maintenance costs associated with your Airbnb rental property.

- Property repair and upgrade: To make your Airbnb rental property profitable, you must sometimes undergo some repairs and upgrades. Needless to say, renovations come with inevitable expenses. Remember, a boost in the vacation property aesthetics and functionality equates to rental business profitability!

- Marketing and advertising: Of course, you want to ensure your Airbnb property gets booked all the time. Robust marketing and advertising can help you skyrocket your Airbnb occupancy rate. However, they sometimes require monetary investments.

- Property Tax: Andrew Pierce, CEO at LLC Attorney, suggests staying on top of your tax obligations. “Sure, they can add up to the expenditures of your vacation property. However, not paying your taxes will lead to legal ramifications and hefty penalties.”

- Property Insurance: Shawn Plummer, the CEO of The Annuity Expert, highlights the importance of getting insurance for Airbnb rental properties. “Not only does it legally protect you from any property liability, but it also prevents you from having financial losses.”

5. Seek and pick the right Airbnb property

Seeking vacation home financing is one thing; looking for the right investment property is another. Before you work with the right mortgage lender, offering the best deal, you must find a property you can afford that’s worth your Airbnb rental business.

Jim Pendergast, Senior Vice President at altLINE Sobanco, recommends doing homework before choosing a vacation property. “You must consider various factors such as the rental market, location, functionality, aesthetics, and competitors. At the end of the day, what good is your vacation home loan if you pick the wrong property? The money you borrowed isn’t worth the property you’ve invested in.”

6. Work with a reliable real estate agent

Real estate, in general, is a complex industry to navigate in. And this applies to the vacation home rental market. On top of that is selecting the right lender and getting the best deal for Airbnb financing. So, what better way to proceed with this endeavor than to hire a real estate agent?

Nathan Smith, CCIM at Austin Tenant Advisors, suggests consulting real estate experts. “You can work with realtors who can help you make informed decisions. They can also refer you to a network of lenders that can offer you the best loan deals. From there, they can help you decide what loan to secure for your investment property.”

Making Your Dream Home Come True through Smart Loan

There’s no denying the value of a vacation property for making your dream of buying a vacation home come true. But before realizing this dream, you ought to apply for a smart loan. As such, home financing with the right lender is key!

As an aspiring Airbnb host, understand what Airbnb financing is and how it exactly works.

To begin, choose one of the financing options discussed above, whether monthly mortgage payments, DSCR loan, HELOC, or small business loan. Likewise, consider the key factors that can impact your funding decisions, such as the down payment, interest rate, repayment terms, and all other requirements.

More importantly, follow our crucial steps for securing the right Airbnb loan. With all these tips and steps, you can ultimately make your vacation rental property dream come true!

![Your Monthly iGMS Roundup [February 2020]](/content/images/size/w600/wordpress/2020/02/igms-roundup-feb-2020-cover.png)